Our Point of View

There is no substitute to common sense fundamental research and hard work in “old fashioned” stock picking and thoughtful portfolio construction. Original research requires dedication, focus and extraordinary creativity.

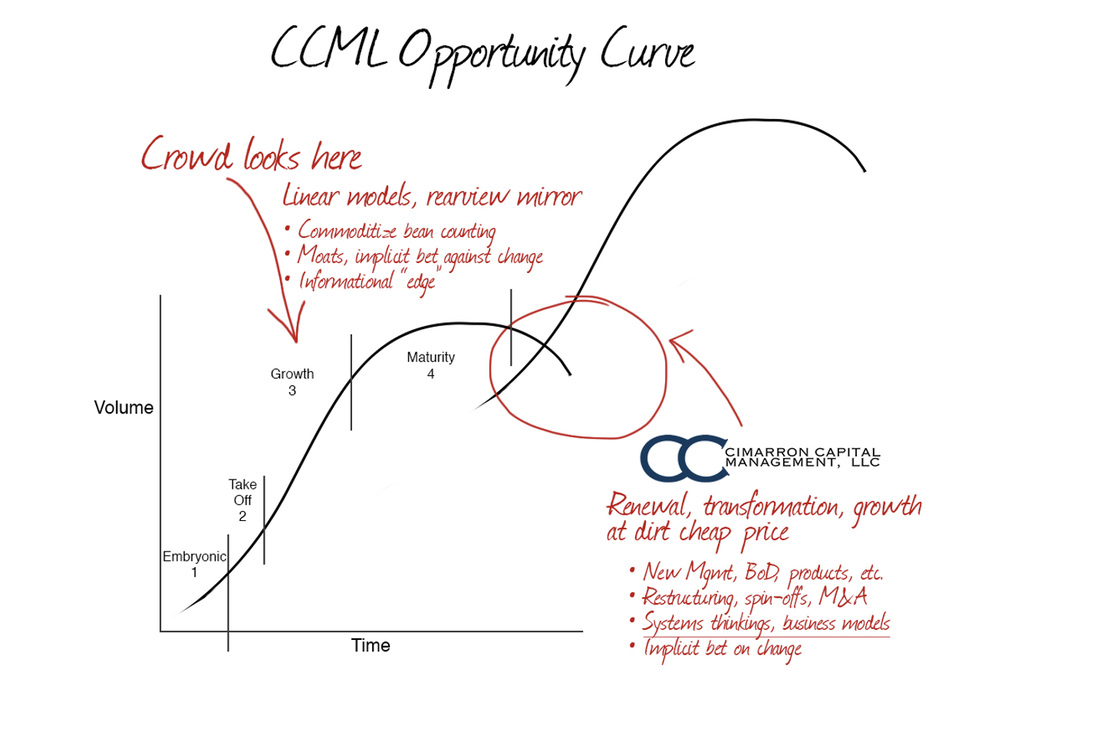

We Embrace Change...

Mainstream analysis focuses on competitive moats protecting the business from competition. We like moats. But in our view moats protect an immovable physical structure––an implicit bet against change.

Betting against change is a non-starter for us. The invaders of technology, demographics and evolving human consciousness have stormed the gate.

We embrace change, renewal and transformation as the primary source of investment opportunity.

Betting against change is a non-starter for us. The invaders of technology, demographics and evolving human consciousness have stormed the gate.

We embrace change, renewal and transformation as the primary source of investment opportunity.

Investment Themes of Focus

Lionhearted gazelles

They are growth companies and founder led businesses. They are bold. Some are too small or lack sufficient trading volume to interest large institutional investors. Optics from reinvestment often obscure attractive long-term business models.

Tigers find their stripes

Small to mid size growth businesses moving up the quality curve. Off balance sheet “hidden” assets are transformed into recognizable income or recurring cash flow on the P&L. We ride on the coattails of change in governance, leadership and renewed capital allocation policy.

Gazelle spirited lions

We often find bargains with “mature” cash rich companies undergoing significant restructuring. They are tackling hard problems today, investing for the future rather than kicking the can to accommodate short-term earnings expectations. They might be rightsizing the balance sheet, selling assets, launching new ventures, spinning off divisions and realigning for sustainable growth.

They are growth companies and founder led businesses. They are bold. Some are too small or lack sufficient trading volume to interest large institutional investors. Optics from reinvestment often obscure attractive long-term business models.

Tigers find their stripes

Small to mid size growth businesses moving up the quality curve. Off balance sheet “hidden” assets are transformed into recognizable income or recurring cash flow on the P&L. We ride on the coattails of change in governance, leadership and renewed capital allocation policy.

Gazelle spirited lions

We often find bargains with “mature” cash rich companies undergoing significant restructuring. They are tackling hard problems today, investing for the future rather than kicking the can to accommodate short-term earnings expectations. They might be rightsizing the balance sheet, selling assets, launching new ventures, spinning off divisions and realigning for sustainable growth.

Sourcing Ideas

Our approach places a strong emphasis on meticulous document research, encompassing a wide array of materials, from books to transcripts and the often-overlooked fine print. The highest quality information is remarkably accessible to anyone possessing the time and patience to unearth it. Our methodology isn't a complex one, but it does require intense focus. In most cases, this contemplative analysis cannot occur within the confines of a conventional office or in front of computer monitors.

Our commitment to due diligence is underpinned by our proactive engagement with a diverse spectrum of stakeholders, including company management, competitors, former employees, and customers, as needed. These interactions serve as invaluable sources of context and validation, enabling us to forge well-informed assessments and make sound decisions.

Paralysis by analysis is a common pitfall in bottom-up strategies. There is always something else to learn about a company. Therefore, it is highly important to recognize that only so much writing, reading, interviewing, and high-level thinking can be done. The key is to know when an accumulated body of knowledge is sufficient, a determination that is more art than science. To this end, I use the Peter Drucker rule: The decision jumps out once the facts are clear.

Portfolio Construction

Portfolios are constructed one stock at a time. No two clients are the same and no two portfolios are identical.

Portfolio weightings, sector allocations, and geographic mix are opportunity dependent. We deviate from popular benchmarks and “style boxes.”

No more than 20 companies. Portfolios are focused on best ideas.

A typical holding period of 2 to 5 years allows for maturation and renewal. However, we are not afraid to sell when the story changes. We optimize for capital appreciation rather than "low turnover".

We invest diversely across various sectors and geographic regions. As global investors, we pursue opportunities rather than adhering strictly to top-down style directives.

Small to mid cap focus, often <$5 billion market valuation on the initial buy.

Portfolio weightings, sector allocations, and geographic mix are opportunity dependent. We deviate from popular benchmarks and “style boxes.”

No more than 20 companies. Portfolios are focused on best ideas.

A typical holding period of 2 to 5 years allows for maturation and renewal. However, we are not afraid to sell when the story changes. We optimize for capital appreciation rather than "low turnover".

We invest diversely across various sectors and geographic regions. As global investors, we pursue opportunities rather than adhering strictly to top-down style directives.

Small to mid cap focus, often <$5 billion market valuation on the initial buy.

Risk Management

Mistakes of judgment and poor timing are part of the game. Discipline helps to reduce the cost.

Purchase: Before a purchase, the investment plan is mapped out on paper, outlining expectations, risks, and contingencies. A brief list of major assumptions, projected outcomes, deadlines, and timelines is developed. This reduces mental load for “sale” decisions.

Evaluate Progress: We maintain consultation with the companies through investor conference calls and direct 1X1 meetings. Regulatory filings, press releases and industry news are monitored daily.

When the reality of the story changes, the investment is revised. Research is ongoing, and investments are hypothesis rather than thesis.

Purchase: Before a purchase, the investment plan is mapped out on paper, outlining expectations, risks, and contingencies. A brief list of major assumptions, projected outcomes, deadlines, and timelines is developed. This reduces mental load for “sale” decisions.

Evaluate Progress: We maintain consultation with the companies through investor conference calls and direct 1X1 meetings. Regulatory filings, press releases and industry news are monitored daily.

When the reality of the story changes, the investment is revised. Research is ongoing, and investments are hypothesis rather than thesis.